At some hazy point somewhere between A-level exams and packing up childhood belongings, thousands of 18-year-olds signed a contract for a Plan 2 student loan. They then hit the road to university with hopes and nerves high in equal measures.

Now, years into adulthood and employment, London graduates are coming to realise the cost of this contract.

Maddie* graduated with an arts degree from a London university in 2018. She now works as a product designer on an annual salary of £60,000. Each month, £236 of her pay cheque goes towards repaying the loan.

But, despite paying back £2,500 since graduating, interest of almost £2,000 leaves her total balance at more than £68,000.

She said: “My remaining balance feels absurd. Even as a relatively high earner, I haven’t even chipped away at it. I’ve paid off £500 in my whole career, as a 30 year old”.

The Rethink Repayment campaign, launched in July 2025, says Plan 2 student loans were mis-sold to a cohort of students over several years. It says the terms of the initial contract have been reneged by consecutive governments, and that young people were given a false impression about the loan from teachers and adults around them.

Maddie added: “It’s frustrating because school didn’t really suggest other options. My school, and I think probably most schools, are under pressure to have figures showing people going to uni, so they push that on students.

“I didn’t feel like I had a choice, so this debt was always something I was going to have to swallow. The loan was framed as being a tax you wouldn’t notice, but that’s not true”.

How do Plan 2 student loans work?

Students have different loan plans depending on where they’re from, the type of course they’re enrolled on and when they started their studies. There are five plans, which vary in terms of interest rates, repayment thresholds, and the length of time before the loan is written off.

Those who received a student loan in England between September 2012 and July 2023, and in Wales from September 2012, are on Plan 2. The rollout of these loans coincided with the tuition fees caps being increased from £3,000 to £9,000 a year.

All graduates on Plan 2 loans pay 9% of their earnings above £28,470/yr towards their debt. This is taken at source, along with income tax and national insurance contributions. The total balance a borrower has to repay is subject to interest, and the rate of this interest varies depending on how much a person earns. The balance is written off after 30 years.

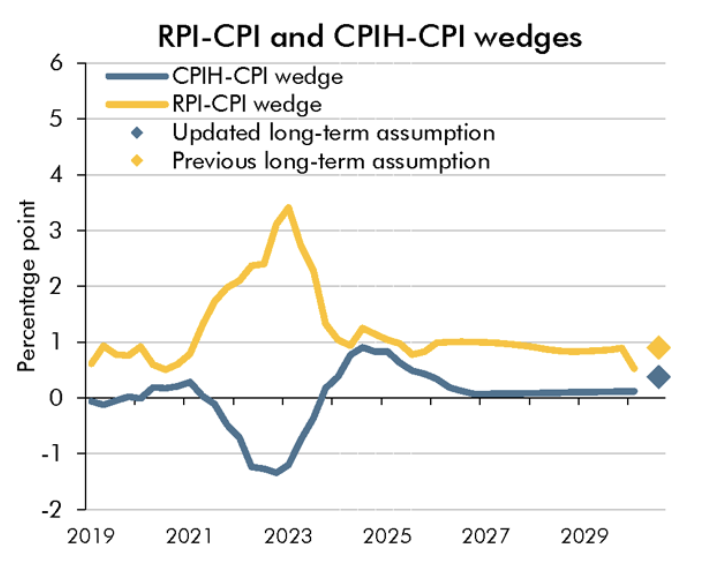

The interest rate consists of two components: the Retail Price Index (RPI) and a real interest rate of up to 3%. RPI is a measure of inflation based on changes to the price of a basket of household items and services. For the period 1 September 2025 to 31 August 2026, the applicable rate of RPI is 3.2%.

Source: Institute for Fiscal Studies

The Office for National Statistics (ONS) discourages the use of RPI to measure inflation, saying: “There are other, better measures available and any use of RPI over these far superior alternatives should be closely scrutinised.” The Office for Budget Responsibility (OBR) estimated RPI to be around 0.9 percentage points higher than the Consumer Price Index (CPI), which is the official measure of inflation.

The real interest rate is applied on top of the rate of RPI. It works on a sliding scale increasing from 0% for incomes of £28,470/yr or less, to 3% for incomes of £51,245/yr or more.

Source: Student Loans Company

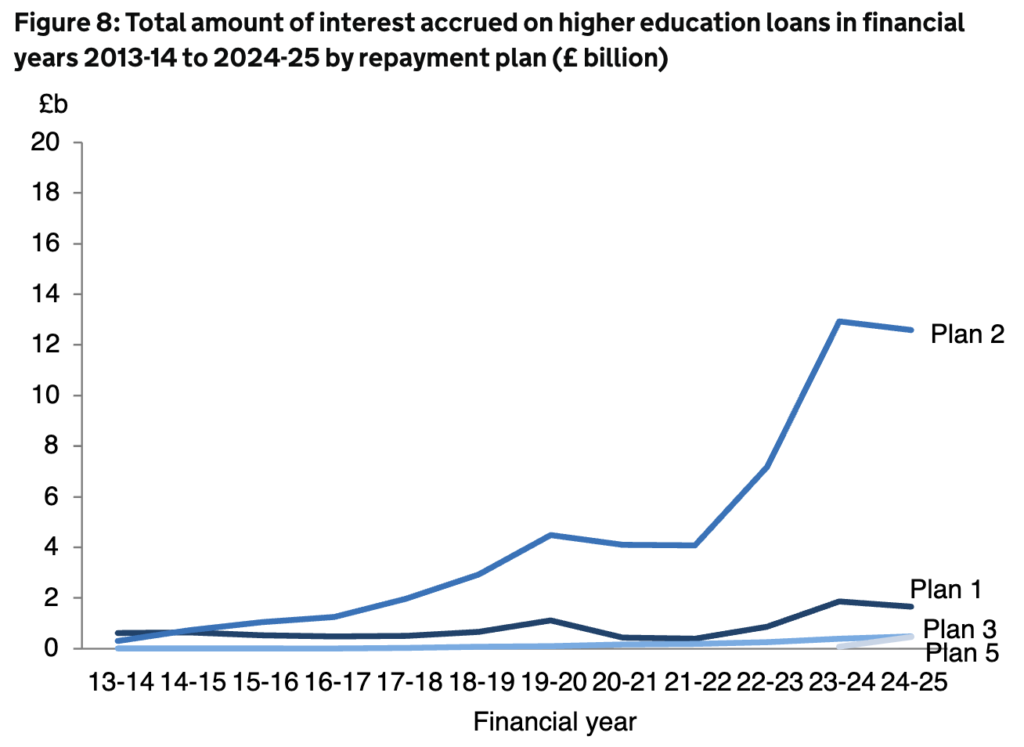

This means that Plan 2 interest accrues at a much higher rate than the other loan plans.The total balance of a loan for someone earning more than the upper thresholds is currently subject to 6.2% interest (RPI 3.2% + real interest 3%).

The increased rate of interest is particularly likely to impact London graduates, where the average professional salaries are higher than elsewhere in the UK.

Director of the Higher Education Policy Institute (HEIP), Nick Hillman OBE, who worked as a specialist education advisor in 2013, told City News: “The Plan 2 student loans in 2012 were very different to Plan 2 student loans in 2026, because, for example, back in 2012 there were still maintenance grants, so we didn’t expect the poorest students to be getting the biggest debts.”

Maintenance grants were replaced with maintenance loans in 2016/17, meaning students would have larger loans to cover their living costs on top of their tuition fees.

Mr Hillman continued: “Back in 2012, the commitment was that the earnings threshold at which you start paying the loan back would rise every year in line with earnings. And that hasn’t happened.”

The government in 2010 stipulated that the payment thresholds for Plan 2 loans would increase “periodically to reflect earnings”, which means the thresholds increase in line with wage growth and inflation. In 2018, increasing these thresholds became a requirement in legislation.

But, in the 2025 Autumn Budget, Chancellor Rachel Reeves said the repayment threshold will increase to £29,385/yr in April, before being frozen at this level until 2030.

Freezing the threshold causes fiscal drag, which is when more of a person’s income will be brought above the threshold as it rises in line with inflation, and therefore subject to the 9% repayment rate. This has previously been branded a “stealth tax”.

The upper and lower thresholds that determine the rate of real interests are also frozen, which the Institute for Fiscal Studies (IFS) says will be more significant for high income earners in the long run.

In 2015, when the then-government introduced a freeze on the repayment threshold, Martin Lewis said: “This retrospective change is a disgrace. No commercial company would be allowed to do it – the Government shouldn’t be allowed to either.” After Mr Lewis threatened the government with a judicial review, it relented and increased the threshold.

‘Squeezed middle’

Former Liberal Democrat leader Sir Vince Cable, who was Business Secretary during the Cameron-Clegg coalition government, told City News that it’s middle earners that are “squeezed” by Plan 2 loans.

He said: “The system has become grossly over complicated and very unfair. The high earners can opt out of the loan scheme by paying cash, the people who are unemployed or low earners don’t pay anything anyway. So it’s the squeezed middle who are feeling the pain.”

“Even people who are earning £50-60,000, that is a good salary, but when you have very high housing costs, and particularly if you’re living in London, you know, it’s not affluent”.

Official portrait of Sir Vince Cable. Image courtesy of Chris McAndrew

James*, who studied at the London School of Economics and now works as a credit analyst at a bank, earned £70,000 last year and paid almost £4,000 on his student loan.

He said: “I keep less than half of any extra money I make over £50,000, which does reduce the incentives to work over-and-above to progress. If I earn an average salary in my career for the next 30 years, I could end up paying back £100,000 for the original £48,000 loan.

“The real high achievers at the bank pay off their student loans early, while some don’t earn enough to get taxed much. I’m in the middle. It wouldn’t make sense for me to try and pay it off”.

“That said, I’m grateful I was able to get a degree for £9,000 a year, when international fees are £39,000.”

‘The system isn’t perfect but it’s progressive’

Mr Hillman told City News that while the system isn’t perfect, it’s “progressive” because those who benefit most from higher education contribute more to its cost.

“If you have a degree, you’re likely to be significantly better paid than people without degrees, and you’re significantly less likely to be unemployed. Taxpayers without a degree shouldn’t have to pay for higher education when they’ve not benefitted from it,” he said.

Nick Hillman OBE. Image courtesy of Higher Education Policy Institute

Lilah*, who graduated as a paediatric nurse from Kings College London on a starting salary below £30,000, said that the problem is not with student loan repayments in isolation, but within a wider context of all rising costs.

She said: “They [the loan repayments] really affected me, especially living in London where the transport is expensive, and the cost of living has increased so much more than wages. In times like this, every little bit counts.”

Mr Hillman also said he thinks it’s the overall economic picture, and factors such as housing, that are really responsible for reducing the standard of living for young people.

“It’s a very difficult time to be young, to get on the housing ladder, to settle down and have kids, but I’m not sure that’s because of our student loan system, but more because of our planning laws and our childcare provisions, things like that,” he said.

Calls for change

The Rethink Repayment campaign proposes three changes: restoring the repayment thresholds to the level they would have been without retrospective changes, cap interest rates at CPI—not RPI—inflation levels and lower the repayment rate from 9% to 5%.

But Mr Hillman told City News: “I still haven’t really heard a sensible solution”. He argued that lowering the repayment rate to 5% would mean the loan is paid off more slowly, causing more interest to accrue.

He also says that removing real interest rates “will do nothing to give you more money in your pocket now”, although it may mean you pay the loan off “a little bit quicker”.

We have contacted Rethink Repayment and the Student Loans Company for comment.

HeadlineDebt is rising faster than London graduates can pay it off: were student loans mis-sold?

Short Headline‘My remaining balance is absurd’: London graduates on the cost of Plan 2 student loans

StandfirstSir Vince Cable told City News that Plan 2 loans are 'unfair', while the Rethink Repayment campaign calls for reform.

At some hazy point somewhere between A-level exams and packing up childhood belongings, thousands of 18-year-olds signed a contract for a Plan 2 student loan. They then hit the road to university with hopes and nerves high in equal measures.

Now, years into adulthood and employment, London graduates are coming to realise the cost of this contract.

Maddie* graduated with an arts degree from a London university in 2018. She now works as a product designer on an annual salary of £60,000. Each month, £236 of her pay cheque goes towards repaying the loan.

But, despite paying back £2,500 since graduating, interest of almost £2,000 leaves her total balance at more than £68,000.

She said: “My remaining balance feels absurd. Even as a relatively high earner, I haven’t even chipped away at it. I’ve paid off £500 in my whole career, as a 30 year old”.

The Rethink Repayment campaign, launched in July 2025, says Plan 2 student loans were mis-sold to a cohort of students over several years. It says the terms of the initial contract have been reneged by consecutive governments, and that young people were given a false impression about the loan from teachers and adults around them.

Maddie added: “It’s frustrating because school didn’t really suggest other options. My school, and I think probably most schools, are under pressure to have figures showing people going to uni, so they push that on students.

“I didn’t feel like I had a choice, so this debt was always something I was going to have to swallow. The loan was framed as being a tax you wouldn’t notice, but that’s not true”.

How do Plan 2 student loans work?

Students have different loan plans depending on where they’re from, the type of course they’re enrolled on and when they started their studies. There are five plans, which vary in terms of interest rates, repayment thresholds, and the length of time before the loan is written off.

Those who received a student loan in England between September 2012 and July 2023, and in Wales from September 2012, are on Plan 2. The rollout of these loans coincided with the tuition fees caps being increased from £3,000 to £9,000 a year.

All graduates on Plan 2 loans pay 9% of their earnings above £28,470/yr towards their debt. This is taken at source, along with income tax and national insurance contributions. The total balance a borrower has to repay is subject to interest, and the rate of this interest varies depending on how much a person earns. The balance is written off after 30 years.

The interest rate consists of two components: the Retail Price Index (RPI) and a real interest rate of up to 3%. RPI is a measure of inflation based on changes to the price of a basket of household items and services. For the period 1 September 2025 to 31 August 2026, the applicable rate of RPI is 3.2%.

Source: Institute for Fiscal Studies

The Office for National Statistics (ONS) discourages the use of RPI to measure inflation, saying: “There are other, better measures available and any use of RPI over these far superior alternatives should be closely scrutinised.” The Office for Budget Responsibility (OBR) estimated RPI to be around 0.9 percentage points higher than the Consumer Price Index (CPI), which is the official measure of inflation.

The real interest rate is applied on top of the rate of RPI. It works on a sliding scale increasing from 0% for incomes of £28,470/yr or less, to 3% for incomes of £51,245/yr or more.

Source: Student Loans Company

This means that Plan 2 interest accrues at a much higher rate than the other loan plans.The total balance of a loan for someone earning more than the upper thresholds is currently subject to 6.2% interest (RPI 3.2% + real interest 3%).

The increased rate of interest is particularly likely to impact London graduates, where the average professional salaries are higher than elsewhere in the UK.

Director of the Higher Education Policy Institute (HEIP), Nick Hillman OBE, who worked as a specialist education advisor in 2013, told City News: “The Plan 2 student loans in 2012 were very different to Plan 2 student loans in 2026, because, for example, back in 2012 there were still maintenance grants, so we didn’t expect the poorest students to be getting the biggest debts.”

Maintenance grants were replaced with maintenance loans in 2016/17, meaning students would have larger loans to cover their living costs on top of their tuition fees.

Mr Hillman continued: “Back in 2012, the commitment was that the earnings threshold at which you start paying the loan back would rise every year in line with earnings. And that hasn’t happened.”

The government in 2010 stipulated that the payment thresholds for Plan 2 loans would increase “periodically to reflect earnings”, which means the thresholds increase in line with wage growth and inflation. In 2018, increasing these thresholds became a requirement in legislation.

But, in the 2025 Autumn Budget, Chancellor Rachel Reeves said the repayment threshold will increase to £29,385/yr in April, before being frozen at this level until 2030.

Freezing the threshold causes fiscal drag, which is when more of a person’s income will be brought above the threshold as it rises in line with inflation, and therefore subject to the 9% repayment rate. This has previously been branded a “stealth tax”.

The upper and lower thresholds that determine the rate of real interests are also frozen, which the Institute for Fiscal Studies (IFS) says will be more significant for high income earners in the long run.

In 2015, when the then-government introduced a freeze on the repayment threshold, Martin Lewis said: “This retrospective change is a disgrace. No commercial company would be allowed to do it – the Government shouldn’t be allowed to either.” After Mr Lewis threatened the government with a judicial review, it relented and increased the threshold.

‘Squeezed middle’

Former Liberal Democrat leader Sir Vince Cable, who was Business Secretary during the Cameron-Clegg coalition government, told City News that it’s middle earners that are “squeezed” by Plan 2 loans.

He said: “The system has become grossly over complicated and very unfair. The high earners can opt out of the loan scheme by paying cash, the people who are unemployed or low earners don’t pay anything anyway. So it’s the squeezed middle who are feeling the pain.”

“Even people who are earning £50-60,000, that is a good salary, but when you have very high housing costs, and particularly if you’re living in London, you know, it’s not affluent”.

Official portrait of Sir Vince Cable. Image courtesy of Chris McAndrew

James*, who studied at the London School of Economics and now works as a credit analyst at a bank, earned £70,000 last year and paid almost £4,000 on his student loan.

He said: “I keep less than half of any extra money I make over £50,000, which does reduce the incentives to work over-and-above to progress. If I earn an average salary in my career for the next 30 years, I could end up paying back £100,000 for the original £48,000 loan.

“The real high achievers at the bank pay off their student loans early, while some don’t earn enough to get taxed much. I’m in the middle. It wouldn’t make sense for me to try and pay it off”.

“That said, I’m grateful I was able to get a degree for £9,000 a year, when international fees are £39,000.”

‘The system isn’t perfect but it’s progressive’

Mr Hillman told City News that while the system isn’t perfect, it’s “progressive” because those who benefit most from higher education contribute more to its cost.

“If you have a degree, you’re likely to be significantly better paid than people without degrees, and you’re significantly less likely to be unemployed. Taxpayers without a degree shouldn’t have to pay for higher education when they’ve not benefitted from it,” he said.

Nick Hillman OBE. Image courtesy of Higher Education Policy Institute

Lilah*, who graduated as a paediatric nurse from Kings College London on a starting salary below £30,000, said that the problem is not with student loan repayments in isolation, but within a wider context of all rising costs.

She said: “They [the loan repayments] really affected me, especially living in London where the transport is expensive, and the cost of living has increased so much more than wages. In times like this, every little bit counts.”

Mr Hillman also said he thinks it’s the overall economic picture, and factors such as housing, that are really responsible for reducing the standard of living for young people.

“It’s a very difficult time to be young, to get on the housing ladder, to settle down and have kids, but I’m not sure that’s because of our student loan system, but more because of our planning laws and our childcare provisions, things like that,” he said.

Calls for change

The Rethink Repayment campaign proposes three changes: restoring the repayment thresholds to the level they would have been without retrospective changes, cap interest rates at CPI—not RPI—inflation levels and lower the repayment rate from 9% to 5%.

But Mr Hillman told City News: “I still haven’t really heard a sensible solution”. He argued that lowering the repayment rate to 5% would mean the loan is paid off more slowly, causing more interest to accrue.

He also says that removing real interest rates “will do nothing to give you more money in your pocket now”, although it may mean you pay the loan off “a little bit quicker”.

We have contacted Rethink Repayment and the Student Loans Company for comment.

A 2024 Freedom of Information request showed Bromley Council had £4.5 million invested in arms companies that year with £1.5 million reportedly linked to Israel.

Undercover officers raided three linked shops in Barking town centre, revealing how illicit tobacco is being hidden in walls, ceilings and nearby locations to evade detection.

More than 330,000 people across the UK sought support from the Stop It Now helpline in 2025 over concerns about their own or someone else’s online sexual behaviour towards children, according to new charity data. The anonymous service says contacts by phone, email and webchat rose significantly over the year.